MARKET INSIGHT

A deep dive look into the sectors

Select a Sector

Industry Mining Downstream – Aluminum

Mining Downstream – Aluminum

MARKET INSIGHT

Segment Rational

RATIONAL

The Aluminium industry is a strategic sector for the Kingdom to grow and further develop, as it serves as an enabler to other sectors (e.g., construction,automotive, renewables, aerospace). Today, KSA’s Aluminium capabilities focus on four product categories: can stock, extrusions, conductor wire, and automotive sheet. However, products like foil, plate, and castings are imported, and some current capacities are projected to be insufficient to cater to increasing domestic demand.

Segment Trends and Value Proposition

SEGMENT TRENDS

Decarbonization.

Energy Reforms.

Digitalization.

Circular Economy.

Drive of China and lightweight materials in Aluminium.

Value Proposition

• In 2019, the global Aluminium consumption reached 66 mn metric tons and is projected to reach 88 mn metric tons by 2030, representing a CAGR of 2.4%.

• KSA market is the largest in GCC, and KSA demand projected to increase from 482 kt in 2019 to 1,129 Metric kiloton in 2030, mainly driven by the ramp up in other high-value-add sectors.

• Integrated value chain from Maaden Al Baitha bauxite mine alumina refinery and finally to downstream activities.

• Vast natural gas availability and low electricity prices.

• High Domestic primary aluminium and bauxite production.

Segment Value Chain

Global Primary Aluminium Production by Region

• To cater the strong demand, production has increased considerably, with China supplying more than 55% of primary aluminium.

Global Primary Aluminium Consumption by Region

• Global Primary Aluminium consumption projected to increase by ~2.5% over next decade with Middle East region growing the fastest at ~5%.

• Global consumption is heavily dominated by the construction and transport sectors which account for ~50% combined .

• China is the biggest exporter of aluminium and aluminium products while the USA and Germany are the largest importers.

Global Aluminium Consumption by Industry

• Globally, construction and transport account for ~50% of the aluminium consumption.

• Share of transport is expected to increase in the future as use of aluminium in automotive is continuously increasing.

• Demand in China and North America is expected to be driven by the automotive industry as manufacturers turn to lighter material.

• Demand in Europe is expected to be driven by the recovery in packaging.

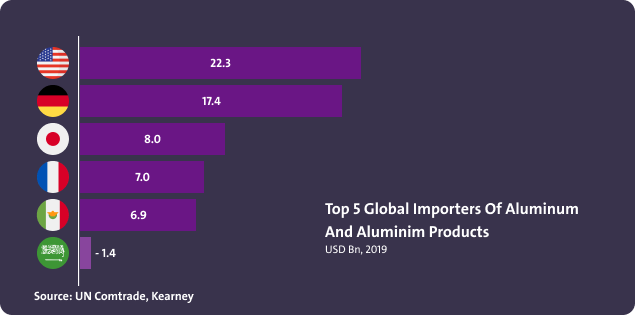

Top 5 Global Importers of Aluminium Products

• USA is the biggest importer of aluminium products, majority coming from Canada, followed by China, UAE and Mexico.

• When combined, European Union members imported USD 25.3 Bn in 2019, excluding intra-regional trade.

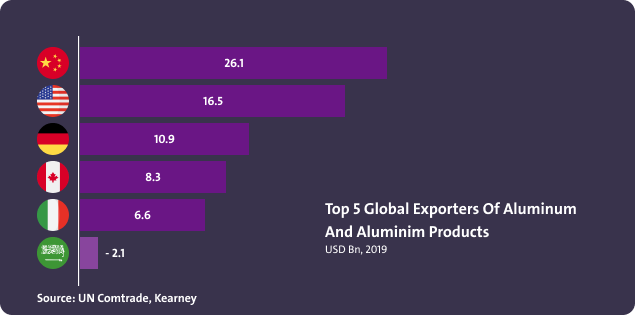

Top 5 Global Exporters of Aluminium Products

• China, accounting for more than half of global primary aluminium production, is the largest exporter of aluminium products.

• The top 3 exporters (China, Germany and USA) represented 31% of global exported volumes in 2019.

Global Cost Curve

However, Saudi Arabia’s low electricity rates leads to an advantageous cost of production, a key benefit for domestic production.

Downstream Aluminium Demand Evolution

By 2030, KSA’s proportional downstream aluminium demand will shift towards extrusions and castings to cater to the automotive, renewables, and aerospace sector.

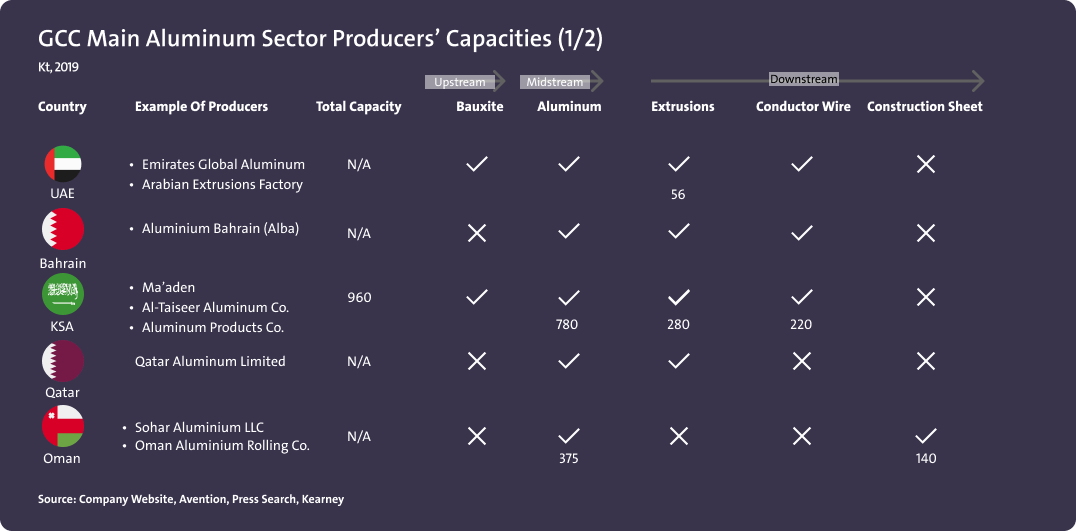

GCC Main Aluminium Sector Producers Capacities (1/2)

All GCC countries operate in the midstream segment of the aluminium value chain while various downstream products are manufactured.

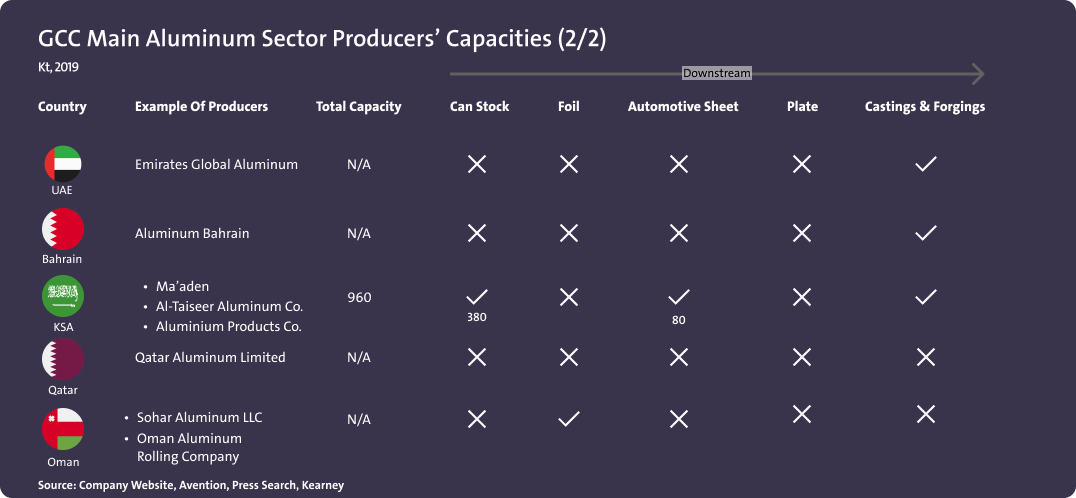

GCC Main Aluminium Sector Producers Capacities (2/2)

All GCC countries operate in the midstream segment of the aluminium value chain while various downstream products are manufactured.

KSA Aluminium Demand by Product Category

Aluminium demand in KSA is expected to experience strong growth in the next decade, mainly driven by the ramp up of the automotive, renewables and aerospace sectors.

KSA FRPs Demand by Product Category

FRPs will see a strong demand from new sectors in the next decade; plates to serve the aerospace sector and sheets to serve the automotive industry.

KSA Exports by Product Category

Imports of extrusions and conductor wire decreased significantly due to lower construction activity while exports of FRPs took off as downstream capabilities increased.

KSA Imports by Products Category

Imports of extrusions and conductor wire decreased significantly due to lower construction activity while exports of FRPs took off as downstream capabilities increased.

Demand and Capacity for Secondary Aluminium Product in KSA

Demand and Capacity for Primary Foundry Alloy (PFA) Product in KSA

Demand and Capacity for Aluminium Foil Product in KSA

Demand and Capacity for Aluminium Plates Product in KSA

Demand and Capacity for Aluminium Extrusions Product in KSA

Demand and Capacity for Castings in KSA

The data and information provided through Daleel platform are for indicative purpose, the provided data and information can be assessed further and analyzed as part of the feasibility studies. In addition, following are other key sources of information that can be used for business case development.

Key Sources for Data

National Geological Database

Reliable national geological and topographic data repository for the whole kingdom of Saudi Arabia including geological and topographic maps, Mineral Occurrences Documentation System (MODS), geochemistry and geophysics data, borehole data, surface samples data and more.

Invest Saudi

For information about investment opportunities in the kingdom to both foreign and domestic investors, as well as private sector businesses please visit Invest Saudi

Tariff Rates and Data

Through the website of the Zakat, Tax and Customs Authority, you can find the tariff rates and data for all kinds of products.

Import Data

Through the website of General Authority for Statistics, you can find detailed data on Import Statistics for all kind of goods.

Export Data

Through the website of General Authority for Statistics, you can find detailed data on Export Statistics for all kind of goods.

Factories Directory

The Factories Directory is provided by the National Industrial Information Center to enable the user to inquire about factories in the Kingdom by activity, production and location, in addition to other data and information.

Ministry of Economy And Planning

A unified platform to present and analyze the latest economic and social the kingdom and its regions in visually interactive ways that facilitate understanding of the Saudi economic landscape.

ZADD

ZAADD is one of the services of the Nine Tenths program launched by the Human Resources Development Fund with the aim of developing small and medium-sized enterprises and making them job-producing institutions. The program also enjoys support from many data-providing entities.