MARKET INSIGHT

A deep dive look into the sectors

Select a Sector

Industry Specialty Chemicals

Specialty Chemicals

MARKET INSIGHT

Segment Rational

RATIONAL

Building on its existing capabilities in Basics and some Intermediate Chemicals, KSA is well positioned to further strengthen its position in the Specialty Chemicals sector by developing and building a sustainable position to become a global and regional leader. Specialty Chemicals represents an attractive opportunity for the Kingdom for two main reasons. The industry can contribute to increasing localization, not only within the Chemicals sub-sectors but also in adjacent industries (e.g., Building Materials, Food Processing, Pharmaceuticals). Specialty Chemicals has also a strong value-adding potential in terms of margins and employment creation; KSA could leverage the growth of Specialty Chemicals to attract talent and technologies.

Segment Trends and Value Proposition

SEGMENT TRENDS

Shifts to tailored end-user products

Stronger IP, formulation, and licensing protection

Focus on sustainability

Disruption of global trade

Value Proposition

• The global Chemicals market is expected to grow at a 3.7% CAGR, doubling production volumes from 1,870 mn ton/year in 2020 to 3,867 mn ton/year by 2040.

• KSA’s Specialty Chemicals industry is expected to grow to 11.5 mn ton/year by 2035.

• Building on its existing capabilities in Basics and some Intermediate Chemicals, KSA is well positioned to further strengthen its position in the Specialty Chemicals sector by developing and building a sustainable position to become a global and regional leader.

Segment Value Chain

MEA and KSA Specialty Chemicals Capacity

Specialty Chemicals segment is expected to almost quintuple the annual growth in regional capacity through 2035.

Global Production of Chemicals Products

• The global chemicals market is expected to grow at 3.7% CAGR, doubling production volumes from 1,870 Mn Ton/year to 3,867 Mn Ton/- year by 2040.

• Chemical sector is also expected to be a driver of demand for oil & gas, gaining share from all other segments, from ~13% in 2020 to ~31% in 2040.

• As oil demand continues to grow but is expected to peak by 2040, chemicals is becoming a most relevant area of focus for O&G countries and companies.

Global Oil and Gas Consumption By Sector (%)

• The global chemicals market is expected to grow at 3.7% CAGR, doubling production volumes from 1,870 Mn Ton/year to 3,867 Mn Ton/- year by 2040.

• Chemical sector is also expected to be a driver of demand for oil & gas, gaining share from all other segments, from ~13% in 2020 to ~31% in 2040.

• As oil demand continues to grow but is expected to peak by 2040, chemicals is becoming a most relevant area of focus for O&G countries and companies.

Comparison of crude oil and natural gas consumption in Saudi Arabia (million tons of oil equivalent)

The Kingdom is home to the Ghawar field, the world’s biggest conventional onshore oil field in terms of reserves and daily output. The oil field has been producing since 1951, and it is estimated to continue pumping oil at its current highest production capacity of 3.8 million barrels a day beyond 2050. Therefore, the country is likely to have a high demand for drilling rigs in the onshore oil and gas operations.

Comparison of crude oil and natural gas reserves in Saudi Arabia (million tons of oil equivalent)

In 2021, Saudi Arabia’s crude oil reserves experienced a slight increase of 0.04%, reaching a total of 37,065 million tons of oil equivalent (TOE) or 267,192 million barrels. However, during the same year, both crude oil production and exports declined. Production dropped by 1.23%, amounting to 462.01 million TOE or 3,331 million barrels, while exports fell by 6.11%, totaling 315.31 million TOE or 2,273 million barrels. This decline was attributed to the economic downturn caused by the global COVID-19 pandemic.

To stabilize crude oil prices, reduce record-high oil inventory levels, and restore global market balance, Saudi Arabia, in collaboration with other OPEC+ members, implemented voluntary production cuts starting in October 2022.

Breakdown Of Chemicals By Major Groups

KSA’s global share in chemicals volume is 4.7%, with a portfolio concentrated in basics and commodity derivatives produced with the gas crackers output.

Market Evolution of Chemical Sales Per Region

Höhepunkte

• Growth is driven by Asia, with China alone owning almost half of the market size of global chemical sales by 2030.

• Market growth in value is higher than global production expansion (in value estimated at CAGR of 5.4%) given that portfolio is steering towards more innovative and higher value-added products.

• Global players must prepare to defend their home markets in downstream, but also to develop export platforms for intermediates and integrated downstream portfolios to better value capture and maintain market positions.

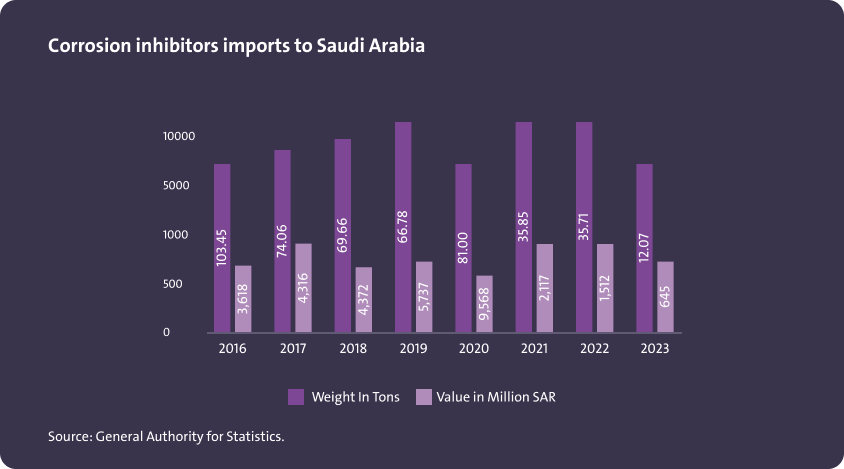

Corrosion inhibitors imports to Saudi Arabia

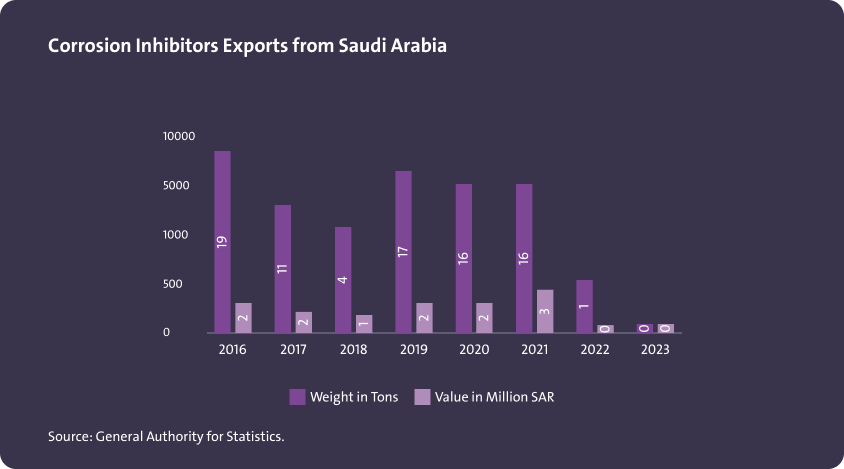

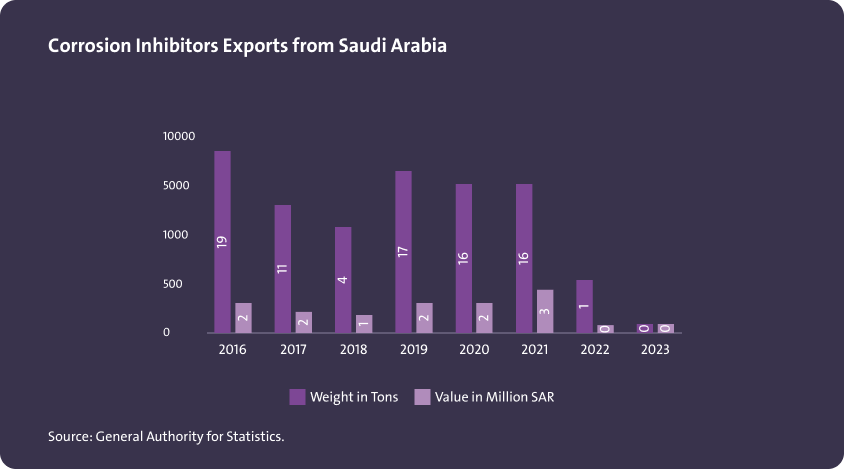

Exports of anti-corrosion and anti-rainfall materials from Saudi Arabia

Saudi Arabia Corrosion Inhibitors Market Size (in Tons)

Corrosion inhibitors imports to Saudi Arabia

Corrosion Inhibitors Exports from Saudi Arabia

Imports of pesticides and disinfectants (biocides) to the Kingdom of Saudi Arabia

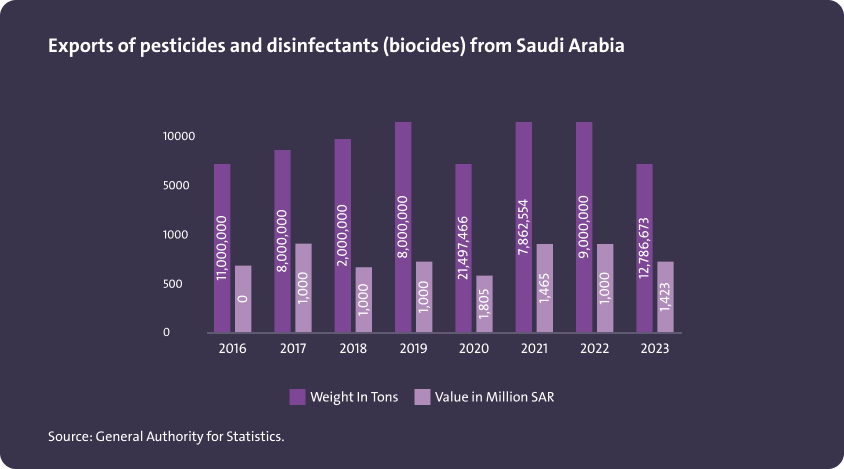

Exports of pesticides and disinfectants (biocides) from Saudi Arabia

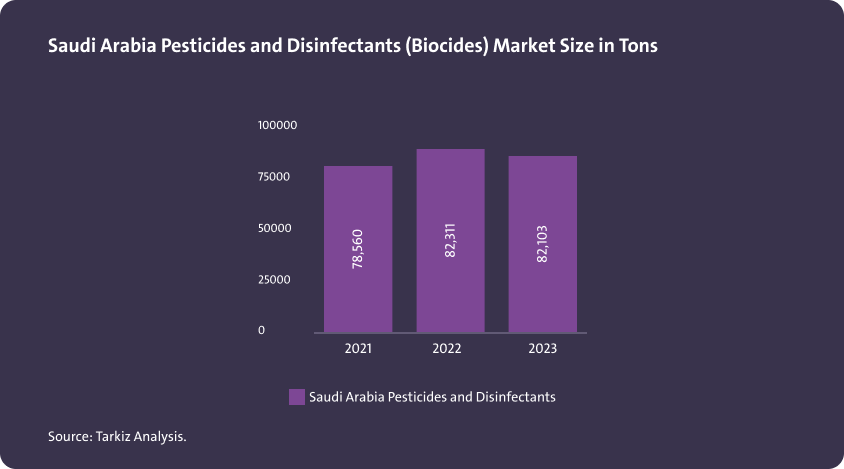

Saudi Arabia Pesticides and Disinfectants (Biocides) Market Size in Tons

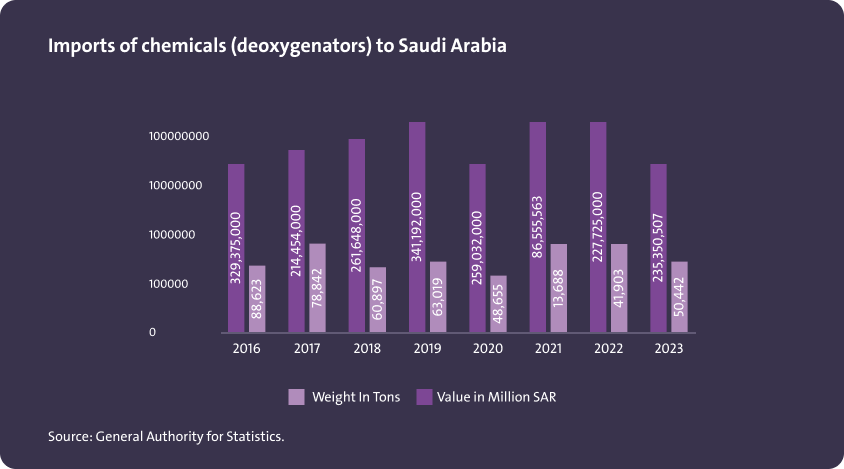

Imports of chemicals (deoxygenators) to Saudi Arabia

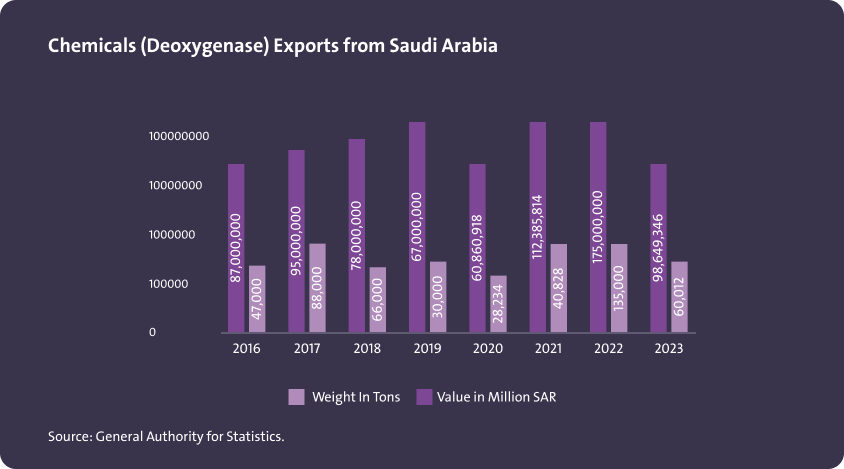

Chemicals (Deoxygenase) Exports from Saudi Arabia

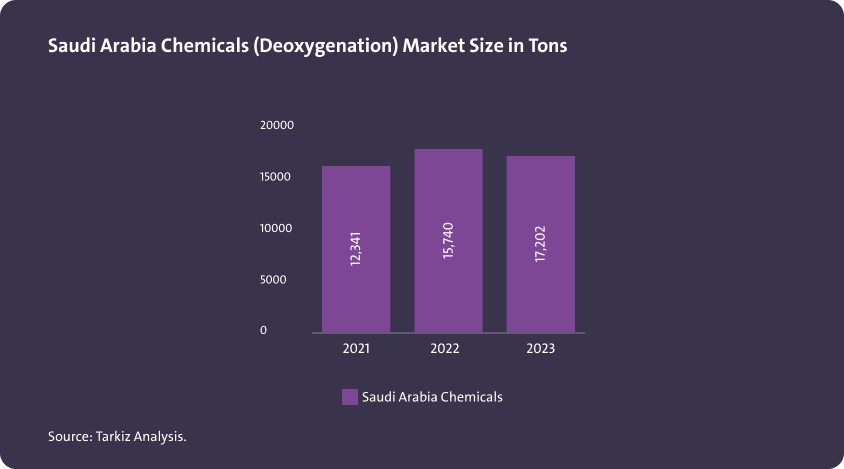

Saudi Arabia Chemicals (Deoxygenation) Market Size in Tons

Graphene import to Saudi Arabia (tons)

Graphene import to Saudi Arabia by country (tons)

Graphene export from Saudi Arabia (tons)

Future demand forecast for graphene in Saudi Arabia (tons)

Adhesive and Sealants KSA Baseline

Catalysts KSA Baseline

Construction Chemicals KSA Baseline

Corrosion Inhibitors KSA Baseline

Flavours and Fragrances KSA Baseline

Food Ingredients KSA Baseline

Industrial and Institutional Cleaners KSA Baseline

Lubricating Oil Additives KSA Baseline

Mining Chemicals KSA Baseline

Oil Field Chemicals KSA Baseline

Paints and Coatings KSA Baseline

Speciality Chemicals for Pharmaceutical Applications Baseline

Plastic Additives KSA Baseline

Market Size For Rubber Processing Chemicals Globally

Specialty Coatings Baseline

Surfactants KSA Baseline

Synthetic Lubricants KSA Baseline

Water Soluble Polymers KSA Baseline

Water Treatment Chemicals KSA Baseline

Antioxidants KSA Baseline

The data and information provided through Daleel platform are for indicative purpose, the provided data and information can be assessed further and analyzed as part of the feasibility studies. In addition, following are other key sources of information that can be used for business case development.

Key Sources for Data

National Geological Database

Reliable national geological and topographic data repository for the whole kingdom of Saudi Arabia including geological and topographic maps, Mineral Occurrences Documentation System (MODS), geochemistry and geophysics data, borehole data, surface samples data and more.

Invest Saudi

For information about investment opportunities in the kingdom to both foreign and domestic investors, as well as private sector businesses please visit Invest Saudi

Tariff Rates and Data

Through the website of the Zakat, Tax and Customs Authority, you can find the tariff rates and data for all kinds of products.

Import Data

Through the website of General Authority for Statistics, you can find detailed data on Import Statistics for all kind of goods.

Export Data

Through the website of General Authority for Statistics, you can find detailed data on Export Statistics for all kind of goods.

Factories Directory

The Factories Directory is provided by the National Industrial Information Center to enable the user to inquire about factories in the Kingdom by activity, production and location, in addition to other data and information.

Ministry of Economy And Planning

A unified platform to present and analyze the latest economic and social the kingdom and its regions in visually interactive ways that facilitate understanding of the Saudi economic landscape.

ZADD

ZAADD is one of the services of the Nine Tenths program launched by the Human Resources Development Fund with the aim of developing small and medium-sized enterprises and making them job-producing institutions. The program also enjoys support from many data-providing entities.